Personalized Financial Literacy at Scale: A GenAI Approach with AI Agents

Revolutionizing Financial Education through AI: Hyper-Personalization and Task-Focused AI Agents

In 2020, I co-authored a material on the following topic - “Broadening the Reach of Financial Literacy Through Hyper-Personalization.” We skewed on the view that it’s better to automate financial decisions on behalf of users given the disparity in understanding of financial topics by individuals. We also counter-argued our view that our approach of ‘doing it for’ users meant the bar to do right by them in all scenarios could not be compromised, not to mention earning users’ trust in all circumstances.

When I revisit this article in 2024, I have a different view!

Today, with developments in Generative AI (GenAI), I have evolved this thinking. We can now build experiences that put users in control.

Behavioral Economics and Financial Literacy

Financial decision-making often portrays irrational behavior influenced by personal circumstances and a limited understanding of financial concepts. Despite the increasing accessibility of financial information and tools, financial literacy remains low.

“On average, American adults correctly answered only 50% of the questions in the 2022 Personal Finance Index, an annual survey conducted by the TIAA Institute and the Global Financial Literacy Excellence Center (GFLEC) at the George Washington University School of Business.” - Source - Yahoo Finance.

Notably, these gaps are even more pronounced among various demographics, including gender, race, and socioeconomic status. For example, studies indicate that men are more likely to be financially literate than women, and significant disparities persist across racial and ethnic groups, with minorities often showing lower financial literacy levels. This ongoing issue underscores the urgent need for innovative approaches to bridge these gaps, as indicated by the options we raise in this article.

Empowered Automation:

We considered merely automating financial decisions on behalf of the user with the shortcomings of financial literacy explained above. GenAI is letting us frame this goal in a completely different light. Instead of purely automating on behalf of the users, we will be able to guide users with insights so they can make sound decisions and have the agents (AI Agents) complete the actions on their behalf (empowered automation).

For instance, if the user reads a headline stating, "Mortgage rates fall from 5.5% to 5%," GenAI can contextualize that with personalized analysis given their unique financial circumstances, including the terms of their current mortgage, cash flow, and goals. As a next step, the agents can assist the user in applying for a mortgage refinance.

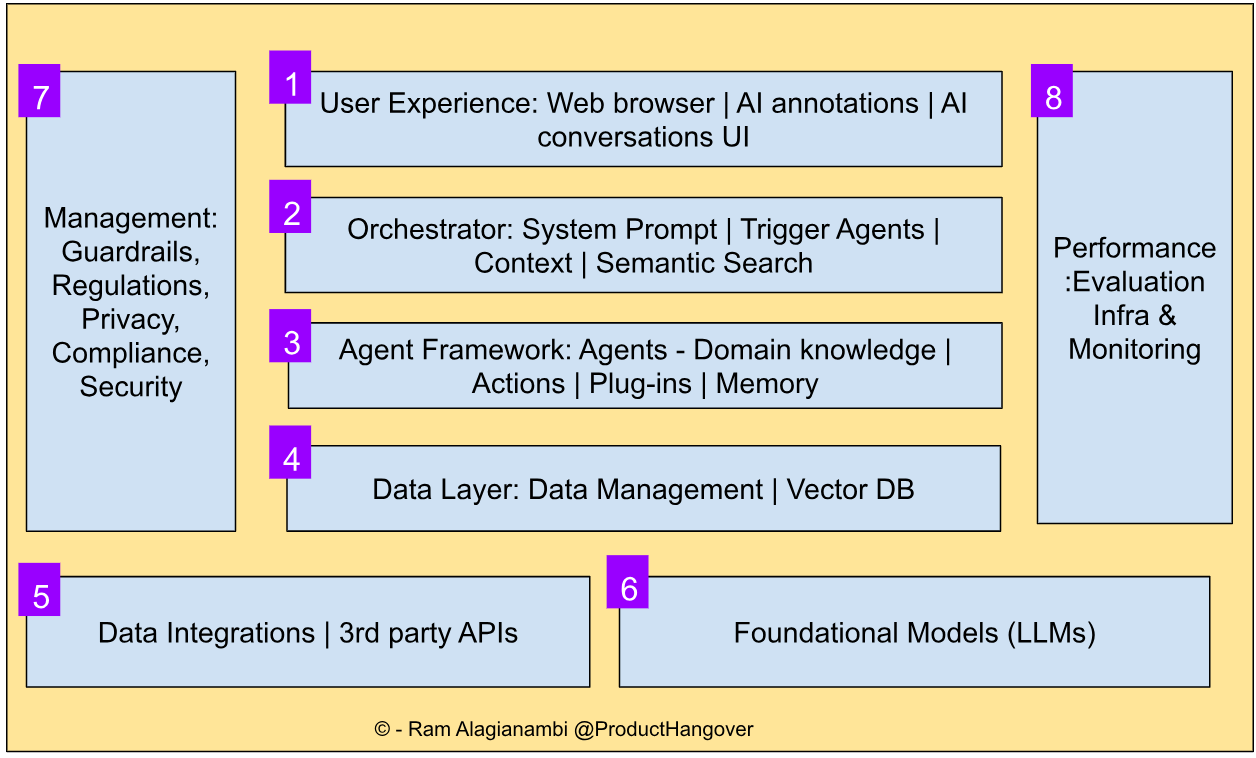

Building Blocks of a GenAI-Powered Financial Assistant

Following are some of the base elements as illustrated in the diagram below:

The above system is agnostic to any domain, be it Finance, Health, Legal, etc.

User Experience:

Features: Integration with a web browser, AI-driven annotation, conversational UI.

Considerations:

Show users how to onboard and self-teach themselves, allowing them to refine the way the AI assistants should work to improve their experience.

The experience can mimic established design patterns, such as annotations on text, chat interface, auto-summarization, and auto-suggestions for the next best action.

Is the browser the super-app that we are overlooking?

Orchestrator:

Role: Ensures the flow of interactions is correctly controlled, the suitable agents are triggered, and semantic search is used for finding relevant context. With models such as o1 from OpenAI, the chain of thought (CoT) is performed on behalf of the user, thereby improving the quality and removing additional work.

Improvements: Real-time data processing and system adaptation based on user input make the whole system responsive and relevant so that the user can get timely and appropriate guidance.

Agent Framework:

Components: A network of domain-specific agents, such as finance, health, etc., along with pre-defined plug-ins and memory so the agents can take actions on behalf of the user.

Considerations: Since agents are regularly updated and maintained, they will follow evolving regulations and market conditions. In addition, these domain-specific models will continue to improve with improvements via training to improve accuracy and lower hallucinations while inference improves performance and cost parameters.

Data Layer:

Components: Data management, vector databases.

Considerations: The Datastore can be used for information on users, their transactions, etc., whereas the Vector DB is a store for indexing and querying vector embeddings. Conversations with customer support and policies from financial institutions can be transformed into relationships and patterns in data and represented as embeddings.

Integrations:

Components: Integration to 3rd party API's and data aggregators like Plaid.

Considerations: This approach overcomes integration challenges and standardization to create a consistent, reliable basis for personalized insights. Agents can be built at this layer to optimize for the best available sources.

Foundation Models

Components: A library of foundational Large Language Models to power the understanding and generation of not only text but audio, video, etc, relevant to financial literacy and user preferences - i.e., what topic is best described using the best modal.

Considerations: Carefully curated and fine-tuned models balance high performance with cost and compliance with financial regulations.

Guardrails

Components: Comprises compliance with regulations, privacy, compliance, and security protocols.

Considerations: This can be further enhanced with real-time monitoring and auditing as part of the comprehensive trust-and-transparency framework.

Evaluation and Monitoring:

Components: Infrastructure for measuring system performance based on user engagement, decision-making accuracy, and conformance to standards. This layer enables continuous improvement in the system, enabling it to evolve to meet users' needs.

The Future of Hyper-personalization

In fact, with the intersection of open banking, GenAI, and improving computing infrastructure, hyper-personalization at scale is just around the corner. Decentralization around financial data empowers users as prime information controllers, granting access only to sources they trust and opening users up to context-aware user-centric tools.

Hyper-personalization can be the next frontier in financial literacy and empowerment. For the first time, with GenAI, users will have at their fingertips the wherewithal to confidently navigate their financial lives and make genuinely informed decisions sans steep learning curves.

Moving toward a world with many more bespoke and user-influenced approaches to making financial decisions strikes a balance between automation and empowerment. With a framework underlining the principles of transparency, compliance, and user-centric design, GenAI potentially further widens that circle of financial literacy and gives users the confidence to make rational decisions.

Here are some additional questions for us to explore:

How do we respect ethical boundaries as we leverage AI to create more immersive user experiences?

Who should be responsible for defining the guidelines that keep AI-driven experiences ethical?

Could the browser be the ultimate super-app, seamlessly integrating AI agents to enhance our digital experiences?